Weekly Market Insights

June 18, 2026 Volume 13 Issue 24

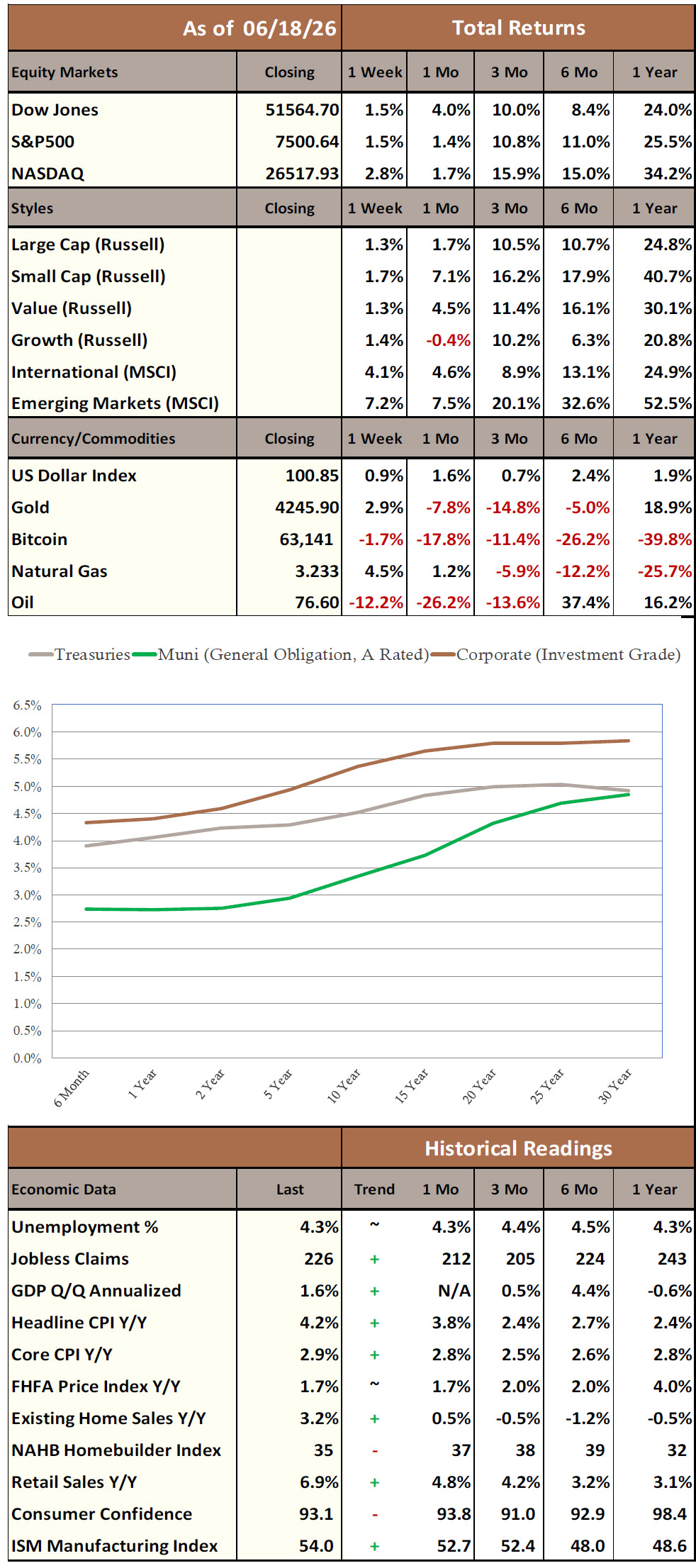

Market leadership was concentrated in U.S. tech and industrials as concerns surrounding the Iran conflict and the Strait of Hormuz eased following the signing of a US-Iran interim memorandum of understanding. Semiconductor stocks led sector performance, with a gauge of chipmakers reaching all-time highs after President Trump announced that Intel and Apple would collaborate on domestic semiconductor design and production, though neither company has officially confirmed. International equity performance was mixed: European financials and industrials set 52-week highs, while the MSCI China index fell more than 2%. Still, MSCI EM stocks gained 7.1% for the week as the US-Iran deal reduced geopolitical risk premia across the asset class. Oil fell sharply. WTI was on track with weekly losses exceeding 13% and approaching pre-war levels.

May CPI rose 4.2% y/y — the fastest pace since early 2023, but in line with expectations, driven primarily by energy costs tied to the war in Iran, though core inflation rose a more modest 0.2% m/m. The labor market remained resilient: initial jobless claims fell to 226,000 for the week ended June 13, and May nonfarm payrolls rose 172,000, above consensus. The central debate focused on whether energy-related price pressures represent a temporary shock — potentially reversing as Hormuz flows normalize, or a more persistent inflation challenge.

The June FOMC meeting — Kevin Warsh’s first as chairman — voted unanimously to hold the benchmark rate steady at 3.5%–3.75%, but the accompanying dot plot signaled a hawkish shift: the median 2026 rate forecast rose to 3.75% from 3.375%, with 9/18 officials projecting at least one hike this year. Warsh used his debut press conference to emphasize the commitment to price stability and announce structural reforms, including a shorter post-meeting statement and task forces to review communications, the balance sheet, and the inflation framework — a deliberate move away from forward guidance toward data dependency. Markets reacted sharply: two-year Treasury yields rose 13 basis points on Wednesday, their largest single-day move since April 2025, as traders priced in rate hikes as soon as July.

Have a great weekend!

The data and commentary provided herein is for informational purposes only. No warranty is made with respect to any information provided. It is offered with the understanding that Hilltop Holdings Inc., PlainsCapital Corporation, Hilltop Securities and PlainsCapital Bank (collectively “PCB”) are not, hereby, rendering financial and/or investment advice, and use of the same does not create any relationship with PCB. This is neither an offer to sell nor a solicitation of an offer to buy any securities that may be described or referred to herein. PCB does not provide tax or legal advice. Please consult your own tax or legal advisor regarding your specific situation. Whether any of the information contained herein applies to a specific situation depends on the facts of that particular situation. Investment and estate planning and management decisions may have significant financial consequences and should be made only after consulting with professionals qualified to offer legal, accounting and taxation advice. Neither this document nor any portion of its content’s supplements, amends or modifies any account agreement with PCB. Unless otherwise noted:

*All economic release data referenced from public sources believed to be accurate. *The source of data for all charts/graphs included in this presentation is Bloomberg LP. *Figures quoted represent monthly changes (m/m) and are seasonally adjusted.