Alternative investments are experiencing a dynamic shift in 2025, marked by high-profile acquisitions, innovative strategies, and emerging opportunities in real assets. These developments highlight both optimism and dispersion in the space under the second Trump administration.

Two significant announcements have underscored the vibrancy of private equity investment. Google’s $32 billion acquisition of cybersecurity firm Wiz represents the largest deal in its history, signaling strong confidence in cloud security and AI-driven services. This acquisition aligns with broader trends in tech-focused private equity, which accounted for over 20% of total buyout value in 2024. The deal reflects optimism about the growth potential of technology, particularly in cloud computing and AI applications.

Similarly, the high-profile bid on the Boston Celtics NBA team by a private equity consortium demonstrates renewed interest in sports franchises as lucrative assets. These megadeals showcase private equity’s adaptability to diverse sectors, buoyed by favorable macroeconomic conditions, including more stable interest rates and anticipation of relaxed regulations under the Trump administration.

Alternatively, vintaged private equity funds are still exploring ways to juggle investor capital beyond recent continuation funds and secondary offerings. Dividend recapitalizations have gained traction as a partial monetization tool, enabling sponsors to extract returns without entirely exiting their investments. This approach increases fund IRR while retaining control over portfolio companies. However, it carries risks, such as heightened leverage and potential default scenarios if companies underperform after the recap. This dispersion reflects varying risk appetites among managers, underscoring the complexity of navigating today’s private equity landscape.

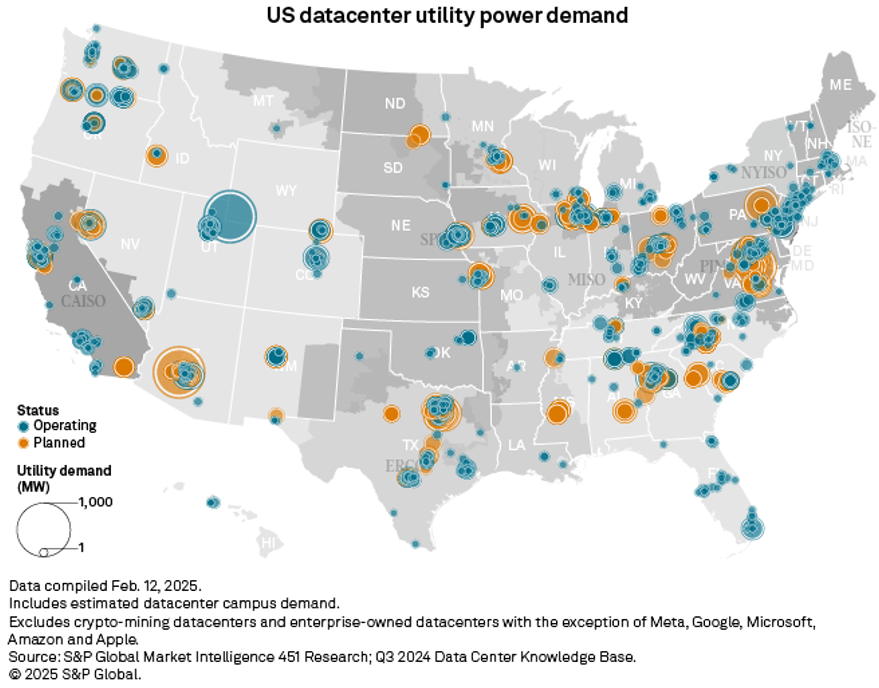

On a different note, the deployment of artificial intelligence is at a nexus with real economy investments, such as natural gas pipelines, utilities, and real estate. Investment opportunities are emerging as physical infrastructure expansion is required to scale up software-driven efficiencies, creating unique investment prospects. For instance, the Stargate Project announced early in the administration that it is looking to develop a data center in Abilene, TX, where Atmos Energy, a Texas natural gas utility, may provide gas, according to S&P Commodity Insights. This gas could be used in collocated generation and consumption by the data center. Such projects offer new investing opportunities spanning several sectors of the economy.

Not to be overlooked, the Trump administration has prioritized cryptocurrency innovation, announcing a strategic reserve in digital assets and appointing officials who are pro-crypto. This regulatory shift aims to position the United States as a global leader in blockchain technology while promoting responsible growth. The reserve has already influenced market sentiment, contributing to price volatility. While the reserve holds seized tokens instead of making purchases, investors nonetheless anticipate more explicit regulatory frameworks. While much still needs to be clarified, cryptocurrencies and their underlying blockchain applications are maturing.

The early months of 2025 showcase a dynamic private equity landscape characterized by optimism; however, like many other asset classes, there remains a significant amount of uncertainty about the longer-term policy landscape. Simultaneously, cryptocurrency developments under the Trump administration add another layer of complexity for investors seeking growth amid evolving regulatory conditions. These are just a few of the trends that collectively highlight the dispersion of opportunities and performance across alternative investments this year. Understanding the role alternatives play in a portfolio, whether as alpha-seeking, income-generating, or diversifying risk exposures, can help investors navigate uncertain times.

ALTERNATIVE PERSPECTIVES