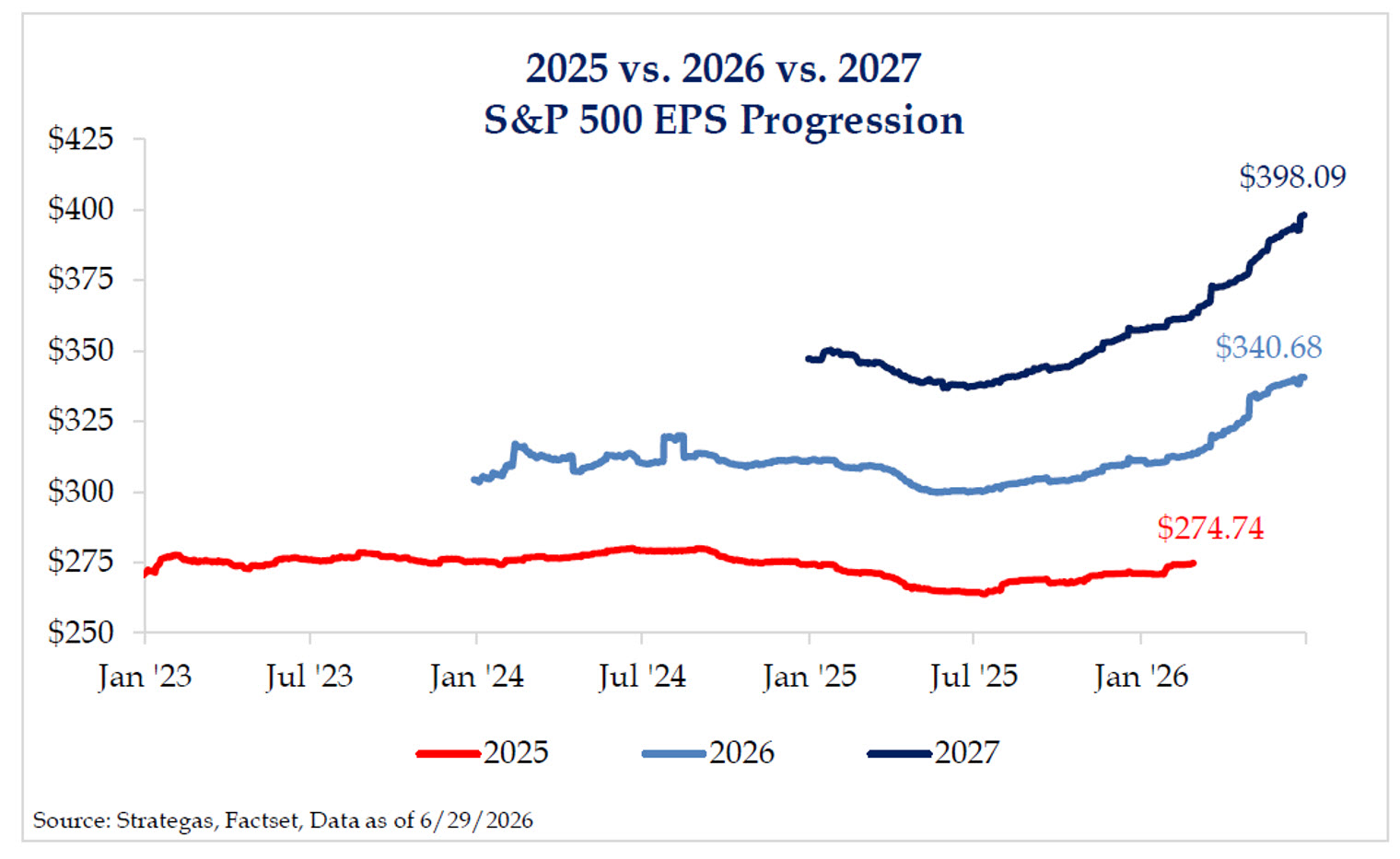

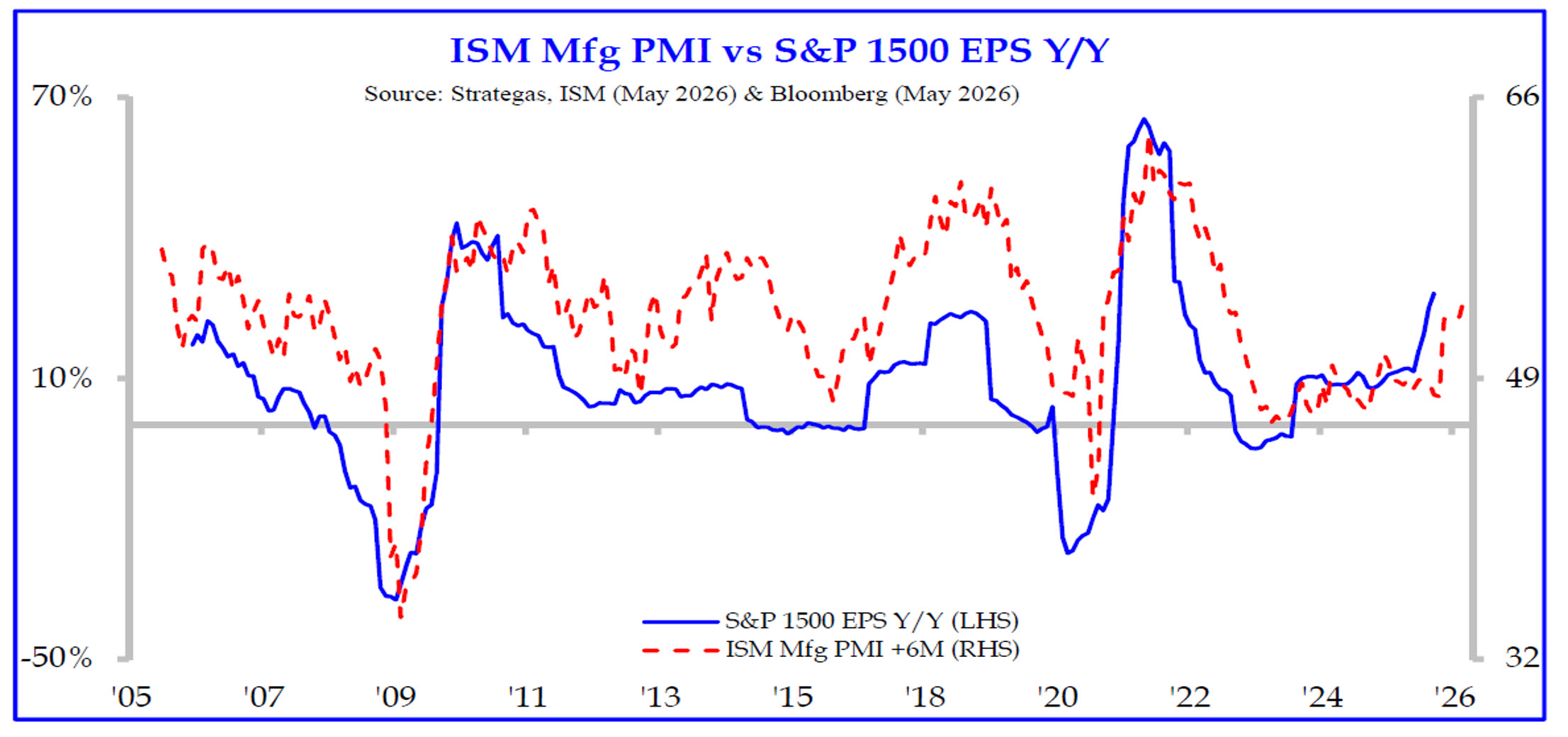

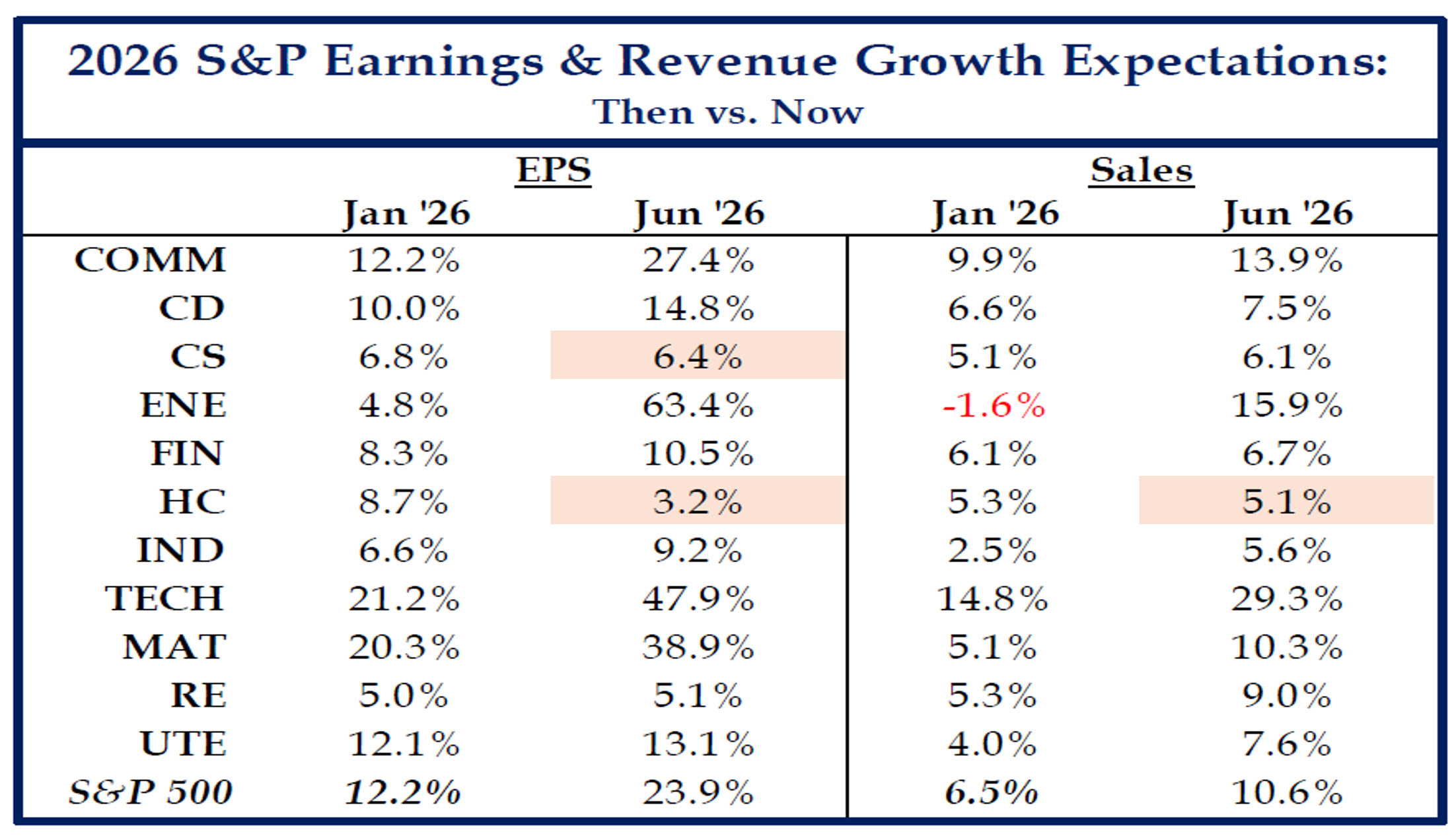

Earnings Expectations Continue to Move Higher: One of the most notable developments in the first half of 2026 has been the continued upward revision of corporate earnings expectations. Analysts have steadily raised forecasts for 2026 and 2027, with technology, communication services, industrials, and materials among the largest contributors. Importantly, earnings strength is no longer confined to a handful of mega-cap technology companies, suggesting that profit growth is becoming increasingly broad-based across the market.

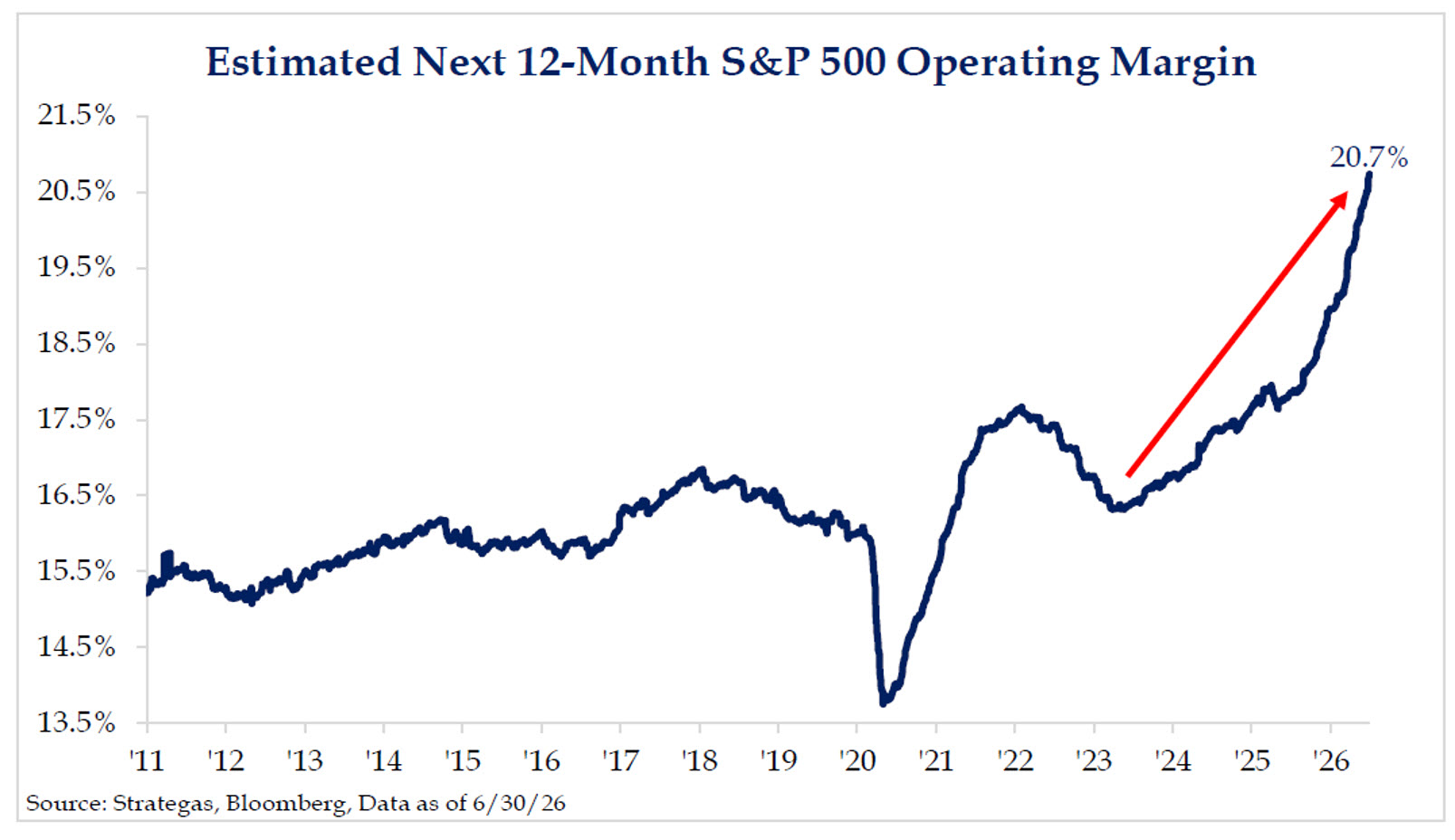

Profit Margins Remain Near Record Levels: Despite concerns surrounding tariffs, labor costs, and geopolitical developments, corporate profit margins remain exceptionally strong. Forward operating margins for the S&P 500 remain near historical highs, reflecting pricing power, productivity improvements, and disciplined expense management. Elevated margins have allowed many companies to absorb cost pressures without materially impacting profitability.

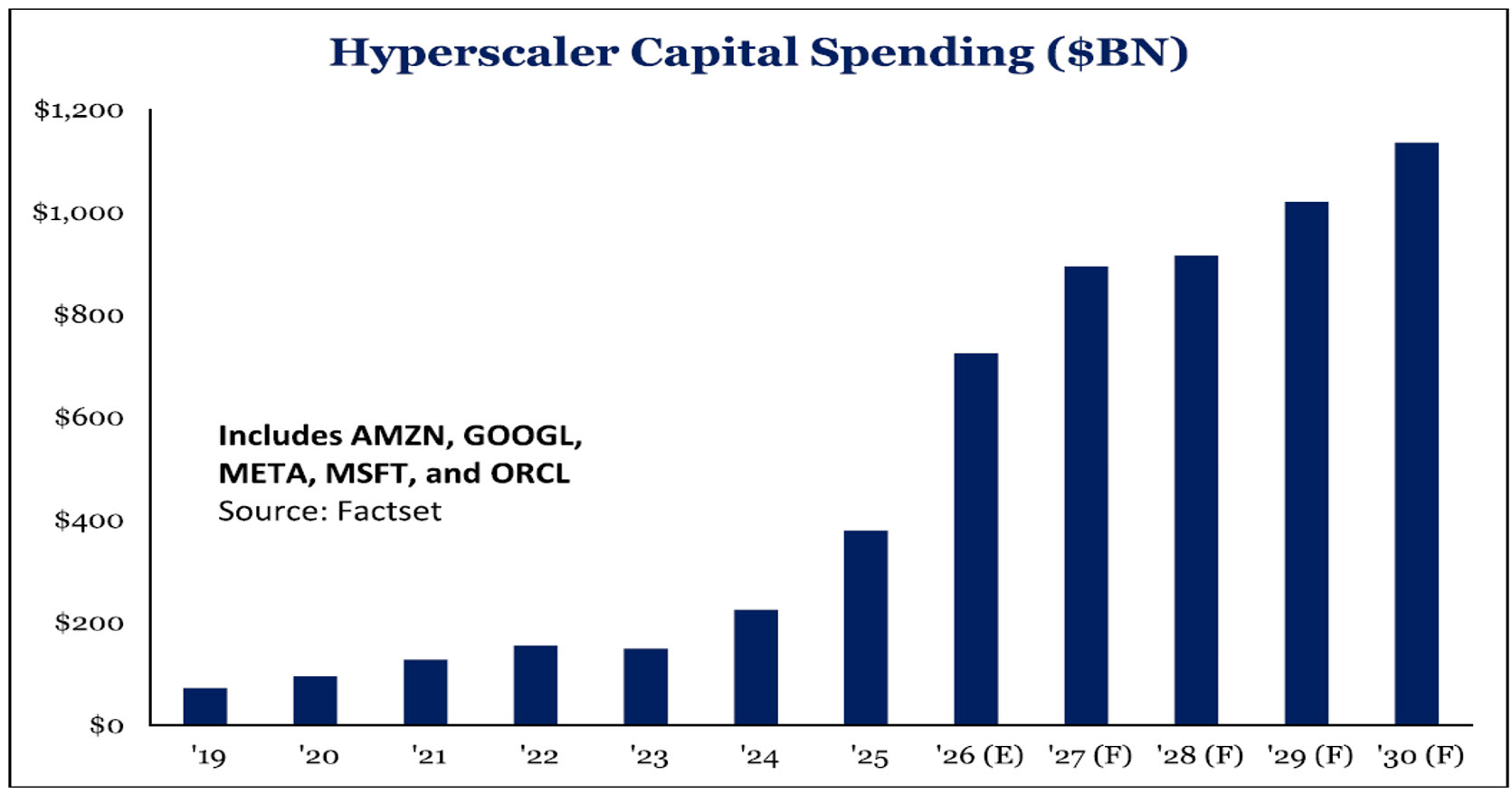

AI Spending Continues to Support Corporate Results: Artificial intelligence remains one of the most important profit drivers across corporate America. Large technology companies, cloud providers, semiconductor manufacturers, and infrastructure suppliers continue to invest aggressively in data centers, computing power, networking equipment, and related technologies. Demand continues to outpace supply in many areas of the AI ecosystem, supporting revenue growth and earnings expansion.

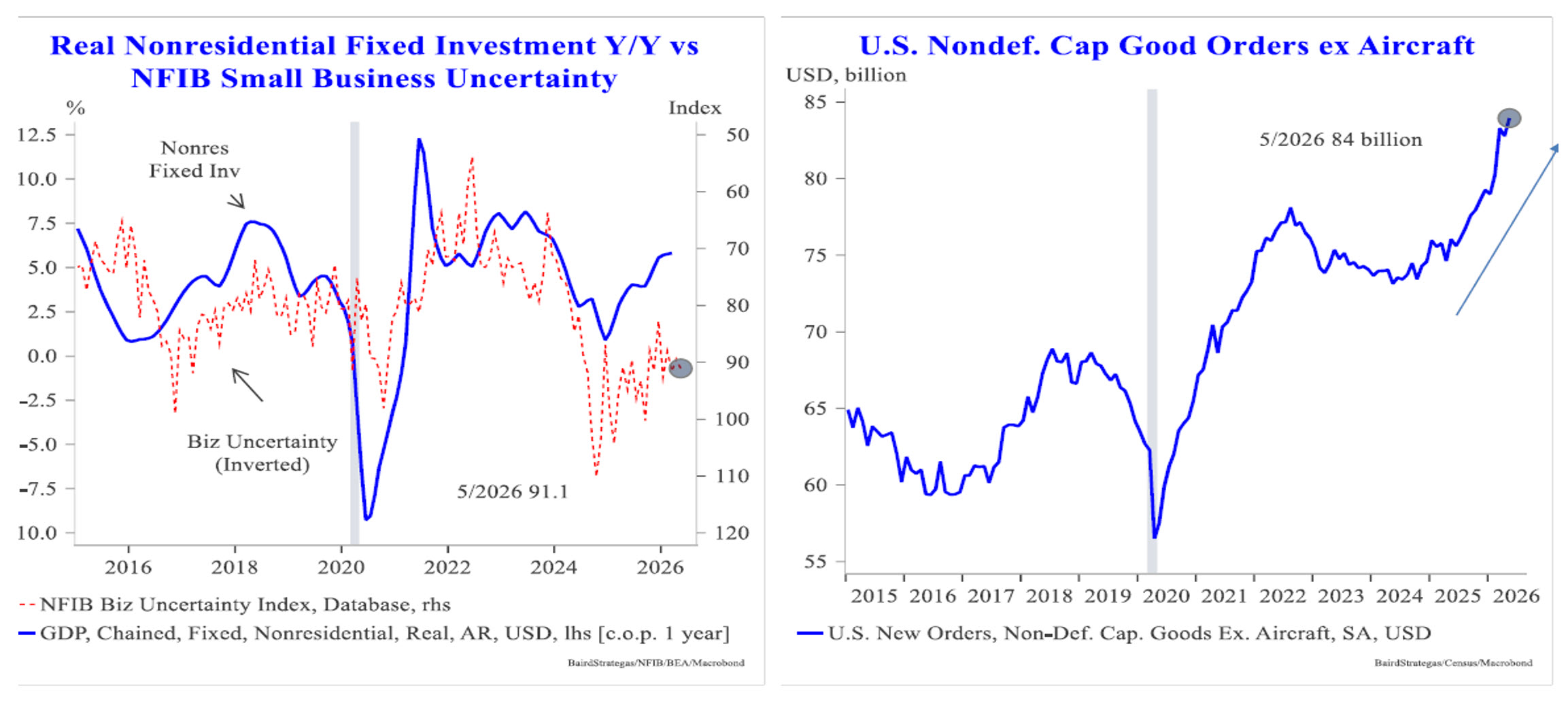

Capital Spending is Supporting Productivity Gains: Unlike prior cycles that relied heavily on consumer demand, the current expansion is increasingly supported by business investment. Spending on technology, automation, manufacturing facilities, and infrastructure can improve productivity and offset rising labor and input costs. These investments provide an important foundation for sustaining profit growth even as economic growth moderates.

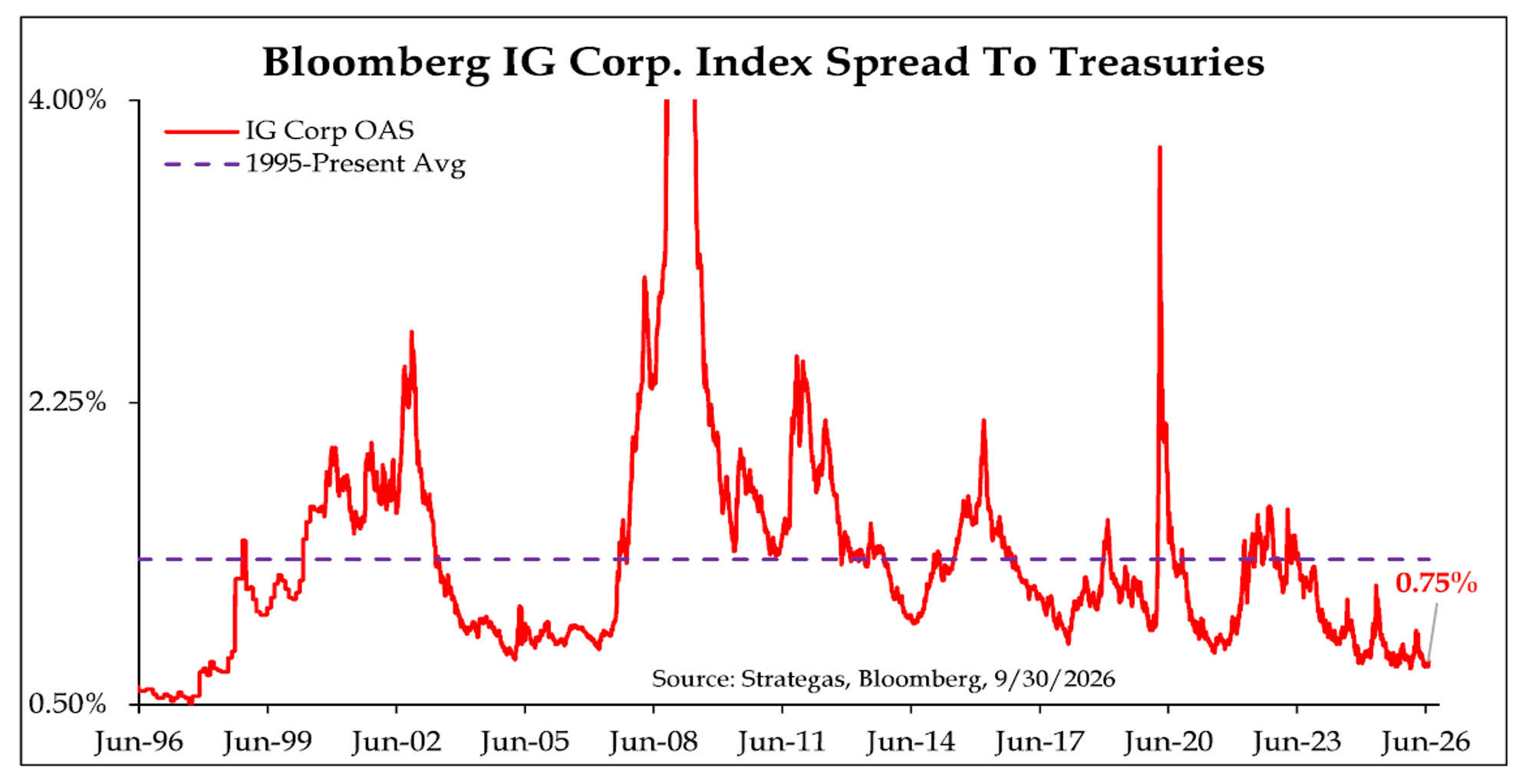

Credit Markets Continue to Support Corporate Activity: Corporate credit markets remain remarkably stable despite concerns about private credit, elevated government borrowing, and higher interest rates. Investment-grade spreads remain tight, credit dispersion is contained, and sector-level bond markets show little evidence of widespread stress. Healthy credit conditions continue to support capital investment, refinancing activity, and shareholder return programs.

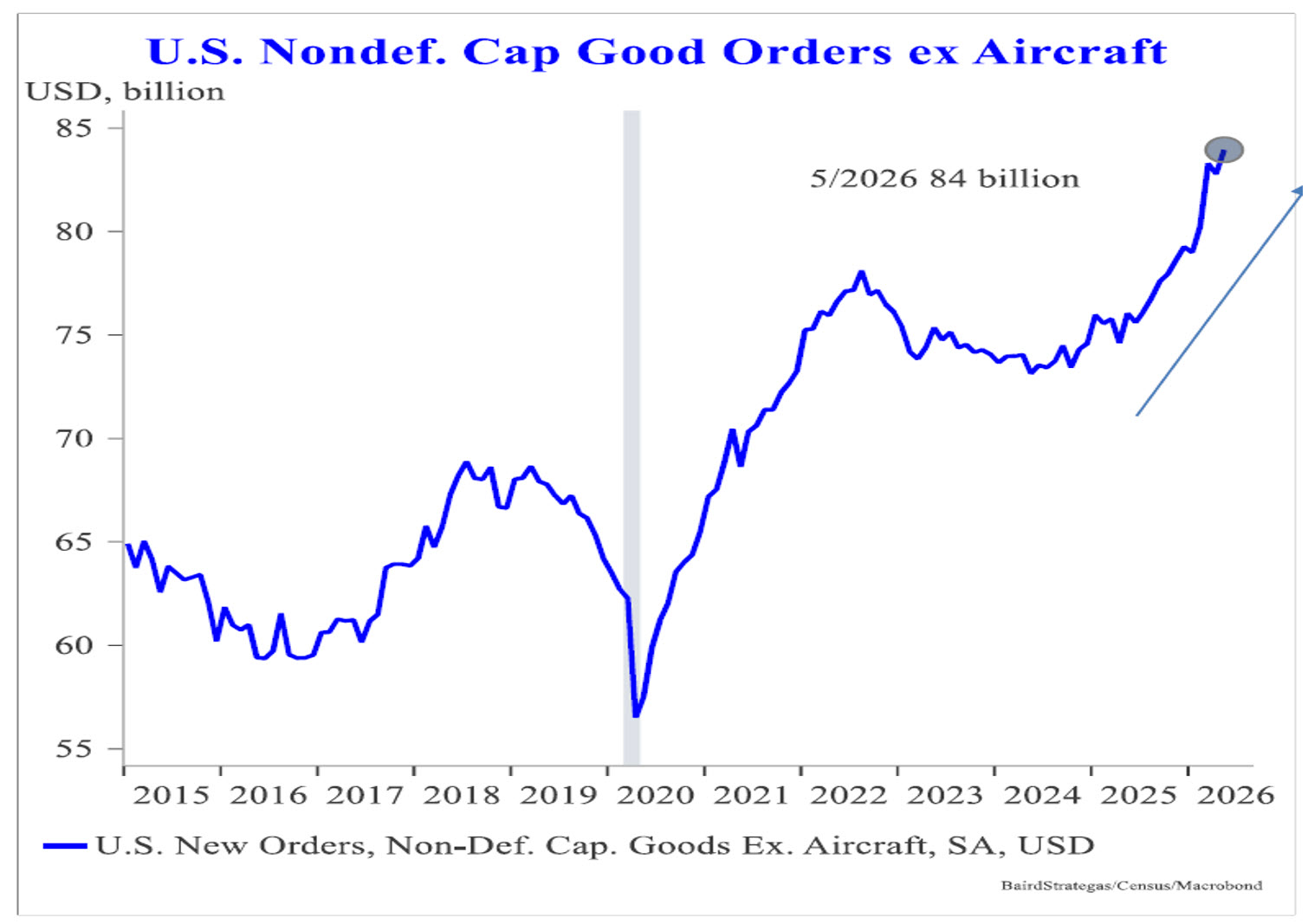

Manufacturing Recovery is Becoming More Meaningful: Several previously weak areas of the economy, including manufacturing and industrial activity, have shown signs of improvement in recent months. Improving factory activity, stronger order backlogs, and increased spending on equipment and technology are helping support earnings growth outside of traditional technology sectors. Broader participation in profit growth is a constructive sign for the durability of the current expansion.

Earnings Growth Remains Inconsistent with A Recessionary Environment: historically, recessions are typically accompanied by deteriorating earnings expectations, widening credit spreads, and contracting profit margins. Current conditions show the opposite trend. Earnings estimates continue to rise, margins remain elevated, and credit markets remain constructive. While economic growth is slowing, corporate profitability data continues to support a base case of continued expansion rather than a recession.

Bottom Line: Corporate America remains a pillar of the economy and financial markets. Strong earnings growth, elevated margins, healthy credit conditions, and ongoing capital investment are helping businesses absorb economic, political, and geopolitical pressures. While growth is likely to moderate from recent highs, current profitability trends remain broadly supportive of continued economic expansion and favorable long-term market fundamentals.

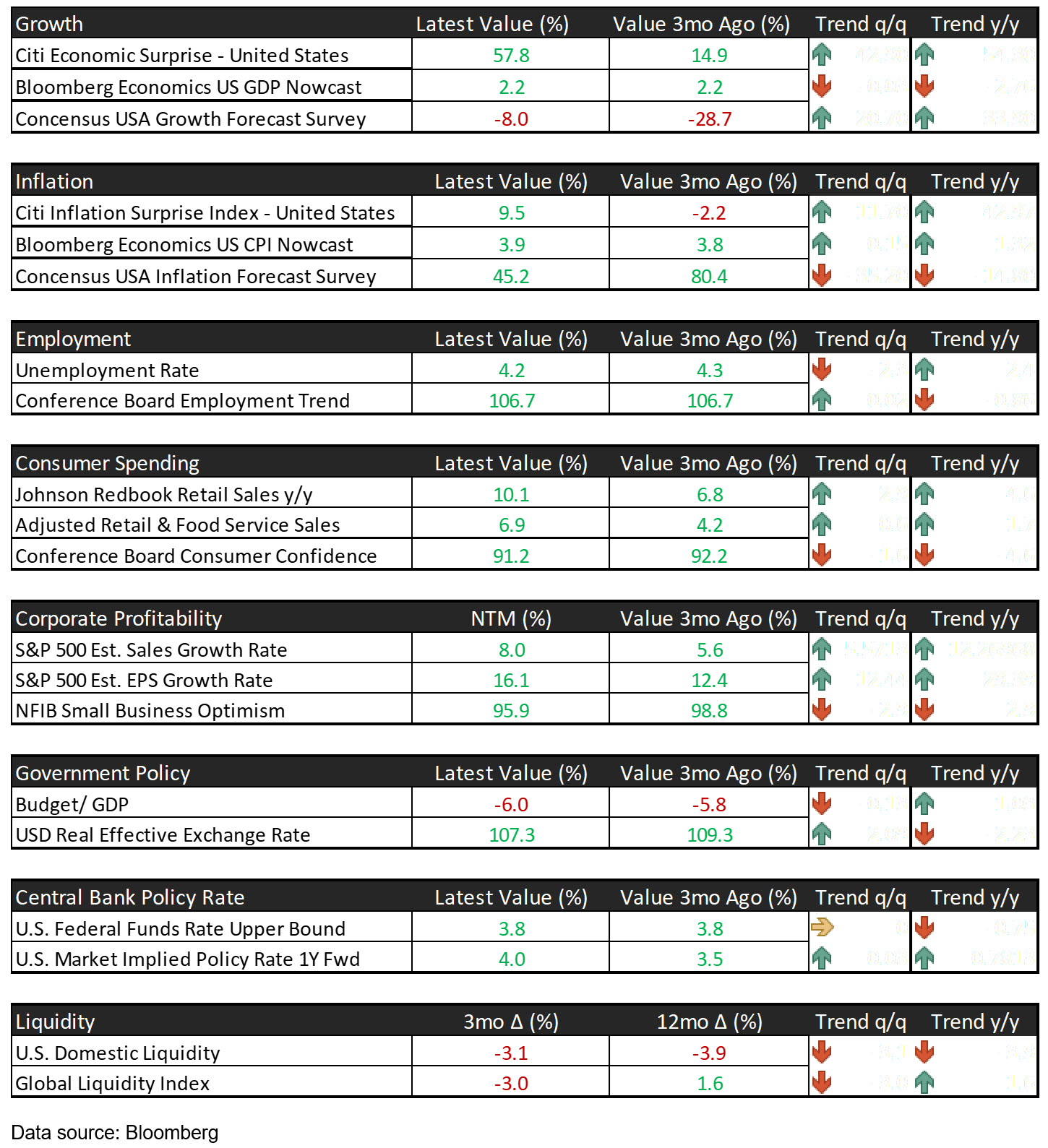

ECONOMIC HIGHLIGHTS