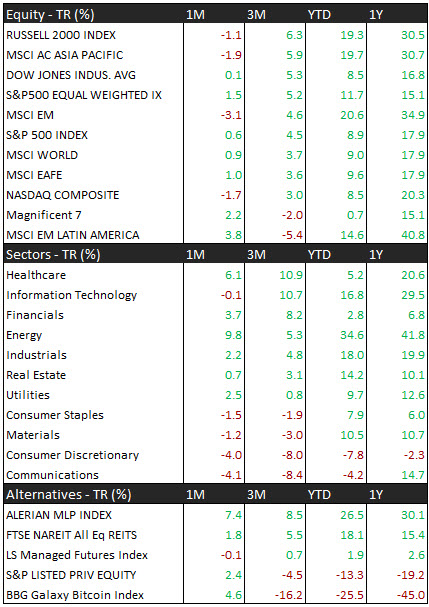

Fixed-income markets remained focused on inflation, monetary policy, and geopolitical developments throughout July, while investors also paid closer attention to technology-sector borrowing in the corporate bond market. Elevated inflation, ongoing energy-related uncertainty, and shifting Federal Reserve expectations continued to influence Treasury yields, credit spreads, and investor risk appetite. Across markets, a common theme has been balancing resilient economic conditions against the risk that inflation remains higher for longer than previously anticipated.

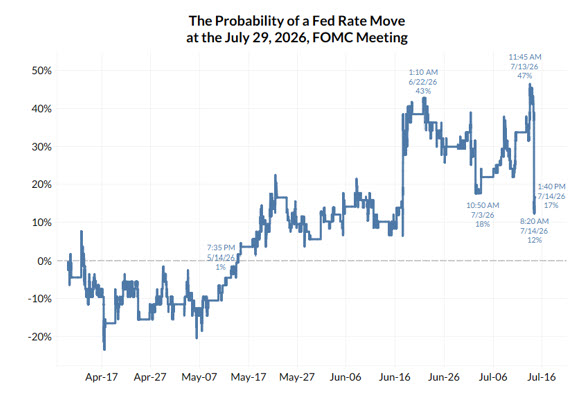

Federal Reserve policy remained the primary driver of fixed-income markets. Fed Chair Kevin Warsh has emphasized price stability as the central bank’s most important objective and has signaled a greater willingness to prioritize inflation risks over labor market weakness. Markets are currently pricing in about a one-in-three chance of a 25-basis-point hike at the July 29 FOMC meeting, with the effective fed funds rate at 3.63%. Significant debate persists over whether further tightening will ultimately be necessary. Recent inflation readings have moderated, but inflation expectations remain above pre-pandemic norms, and policymakers appear determined to avoid repeating past mistakes that allowed inflation pressures to become entrenched. Some market participants believe the economy is slowing sufficiently to reduce the need for additional tightening, creating a meaningful divergence between market pricing and several leading fixed-income outlooks.

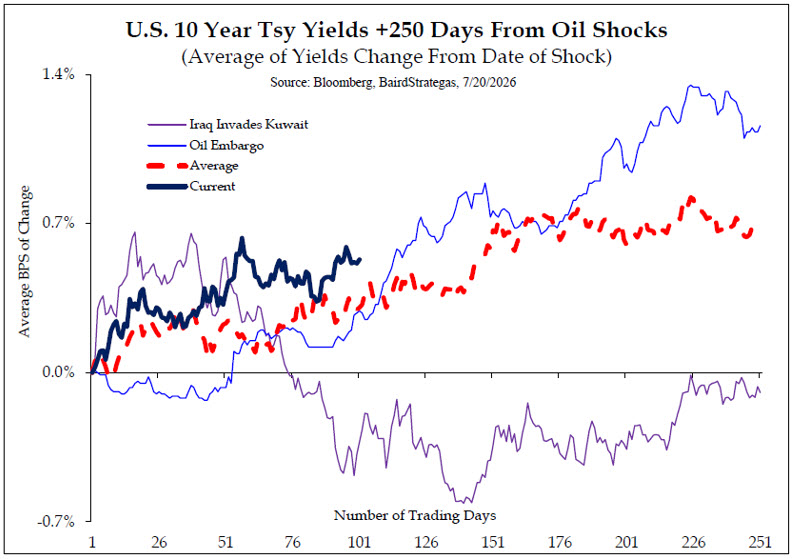

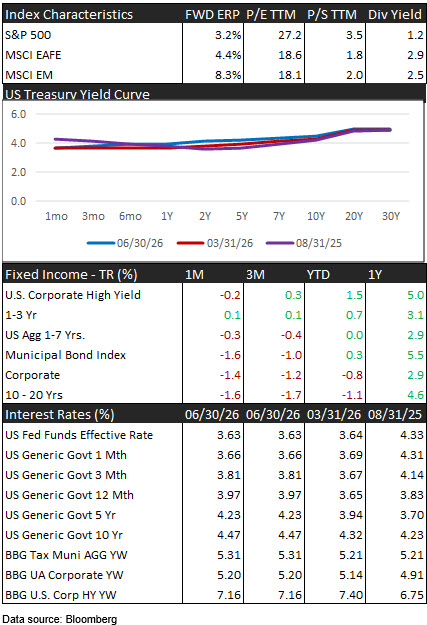

Treasury markets reflected this uncertainty through elevated yields and ongoing debate over the shape of the yield curve. The 10-year Treasury yield rose about 21 basis points in July to 4.695%, as investors reassessed the pace and timing of potential policy easing. Expectations for future Fed policy remain concentrated in short- and intermediate-term maturities, while longer-term yields continue to respond to inflation expectations, commodity prices, and concerns about fiscal conditions. Although some observers expect yields to decline as growth moderates gradually, others note that bond markets continue to behave more like those in historical periods marked by prolonged energy shocks than by temporary disruptions.

Credit markets have remained broadly resilient, with spreads at historically tight levels rather than deteriorating as some commentary suggested. The Bloomberg U.S. Corporate High Yield OAS stands at 276 basis points as of July 23, having traded in a narrow range of approximately 257 to 282 basis points over the past three months. These levels remain well below those associated with prior periods of significant financial stress. While some differentiation is emerging between higher- and lower-quality issuers, the overall picture reflects continued investor confidence in corporate fundamentals rather than broad credit deterioration. The trend warrants monitoring, but current spread levels do not signal elevated systemic risk.

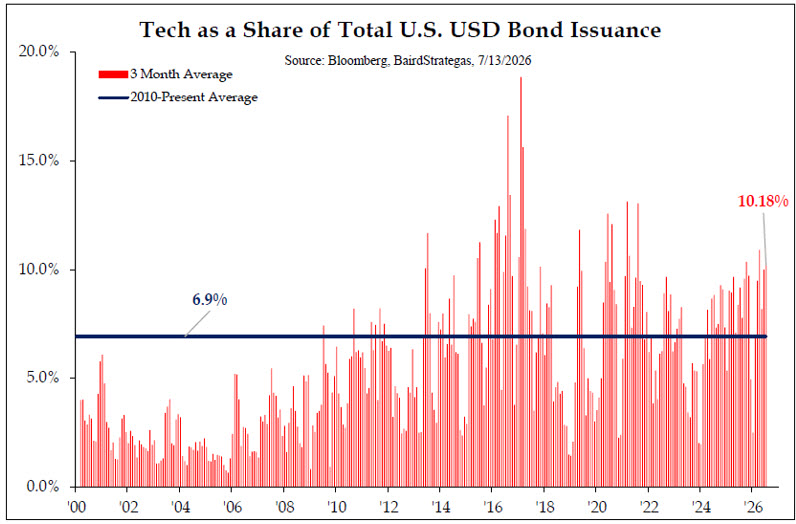

Technology-sector debt has become a notable component of the corporate bond market. Technology companies accounted for approximately $119.9 billion of investment-grade issuance in 2026, representing roughly 4.6% of total IG supply of about $2.6 trillion. Investors are beginning to focus on a potential maturity concentration in technology-related debt later this decade, when a meaningful volume of AI-infrastructure-linked borrowing may need refinancing. The sector’s ability to demonstrate sufficient returns on substantial AI-related investments may become increasingly important as refinancing needs approach, particularly if borrowing costs remain elevated.

Looking ahead, the fixed-income outlook remains centered on inflation, Federal Reserve policy, and the persistence of economic growth. Opportunities remain in high-quality fixed-income sectors, where yields continue to offer attractive income relative to recent history. Risks include renewed inflation pressures, further increases in commodity prices, and policy actions that could keep rates elevated longer than expected. At the same time, stable growth, anchored long-term inflation expectations, and resilient corporate fundamentals — reflected in historically tight credit spreads — continue to support fixed-income investors. As the second half of the year unfolds, the interplay among inflation trends, credit conditions, technology-sector borrowing, and Federal Reserve decisions will remain critical determinants of fixed-income performance.

Sources: 3Fourteen Research, Strategas Research Partners, Bianco Research, Bloomberg, FRED, St. Louis Federal Reserve Bank

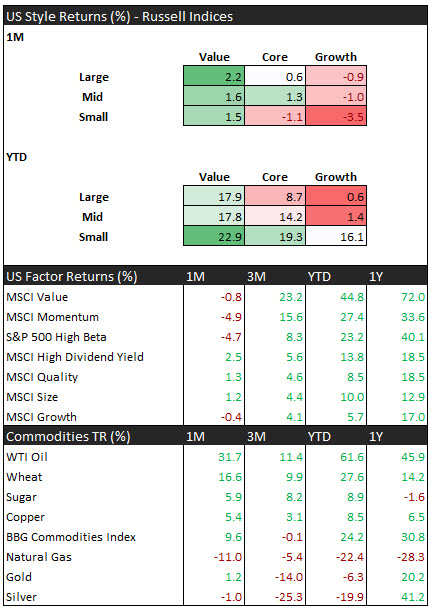

MARKET HIGHLIGHTS