Weekly Market Insights

August 3, 2026 Volume 13 Issue 29

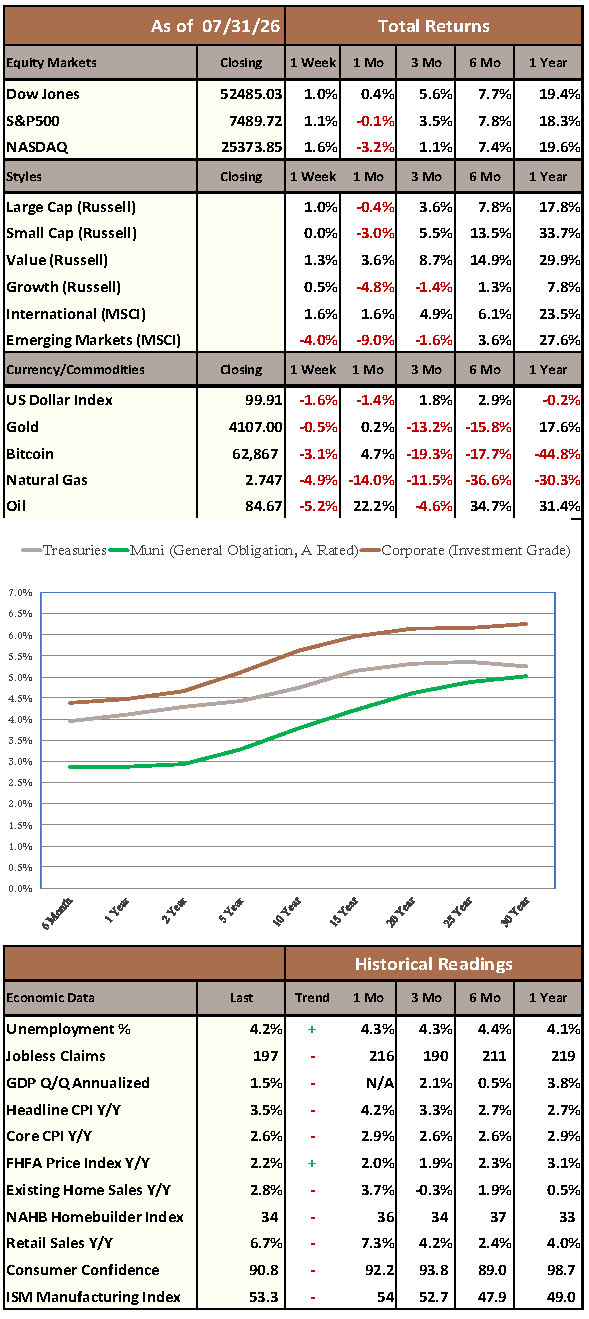

Market leadership broadened during the week ending July 31, though technology remained a significant contributor. Consumer discretionary (+3.66%) and health care (+3.03%) led S&P 500 sector performance, followed by communication services (+2.50%) and information technology (+1.82%). Microsoft’s approximately 16% single-day gain on July 30 — the largest single-day market-cap increase in stock market history — was a notable driver within technology. Large-cap value outperformed growth for the week, with the Russell 1000 Value Index returning +1.41% versus +0.57% for the Russell 1000 Growth Index. Developed international equities advanced, while emerging markets declined for the week despite a sharp Friday rally fueled by AI optimism and a record gain in South Korean equities.

The Treasury yield curve steepened after the Federal Reserve’s policy announcement, with the 2-year yield down about 5 basis points and the 10-year yield up about 7 basis points. Shorter-maturity and high-yield corporate bonds posted modest gains. Commodities broadly declined, with the Bloomberg Commodity Index down about 2.1% for the week, though oil prices were volatile — Brent crude fell sharply on Monday before recovering to post its largest monthly gain since March.

Monetary policy was the defining theme of the week. The Federal Open Market Committee voted 9-3 to keep the benchmark federal funds rate in a range of 3.5% to 3.75%, with Dallas Fed President Logan, Cleveland’s Hammack, and Minneapolis Fed chief Kashkari dissenting in favor of a quarter-point increase. Chairman Warsh continued to reduce forward guidance, prompting markets to assess economic conditions more independently.

Corporate earnings remained in focus, as AI-related capital spending, valuations, and financing costs drew increased investor scrutiny. The week’s rotation — described as the largest since 2020 — reflected a growing debate over AI crowding risks, alongside persistent inflation pressures and geopolitical tensions.

Have a great week!

The data and commentary provided herein is for informational purposes only. No warranty is made with respect to any information provided. It is offered with the understanding that Hilltop Holdings Inc., PlainsCapital Corporation, Hilltop Securities and PlainsCapital Bank (collectively “PCB”) are not, hereby, rendering financial and/or investment advice, and use of the same does not create any relationship with PCB. This is neither an offer to sell nor a solicitation of an offer to buy any securities that may be described or referred to herein. PCB does not provide tax or legal advice. Please consult your own tax or legal advisor regarding your specific situation. Whether any of the information contained herein applies to a specific situation depends on the facts of that particular situation. Investment and estate planning and management decisions may have significant financial consequences and should be made only after consulting with professionals qualified to offer legal, accounting and taxation advice. Neither this document nor any portion of its content’s supplements, amends or modifies any account agreement with PCB. Unless otherwise noted:

*All economic release data referenced from public sources believed to be accurate. *The source of data for all charts/graphs included in this presentation is Bloomberg LP. *Figures quoted represent monthly changes (m/m) and are seasonally adjusted.